South Korea's AI Market Today — Where to Double Down, Where to Rethink

Korea’s AI: #1 in Chips — But Where Does It Stand in AI?

South Korea leads the world in memory semiconductors, displays, and shipbuilding, among other industries. But where does it stand in AI? For now, the country appears to be a dominant supplier of critical components, yet with limited presence in models, platforms, and applications.

SK hynix and Samsung Electronics supply 98% of the HBM (High Bandwidth Memory) used in NVIDIA’s H100. Korea manufactures the core building blocks of AI infrastructure — but its footprint in the models, platforms, and applications running on top of that hardware remains thin.

This post diagnoses the Korean AI market sector by sector, distinguishing areas where real competitiveness can be built from those where the return on investment is likely to fall short.

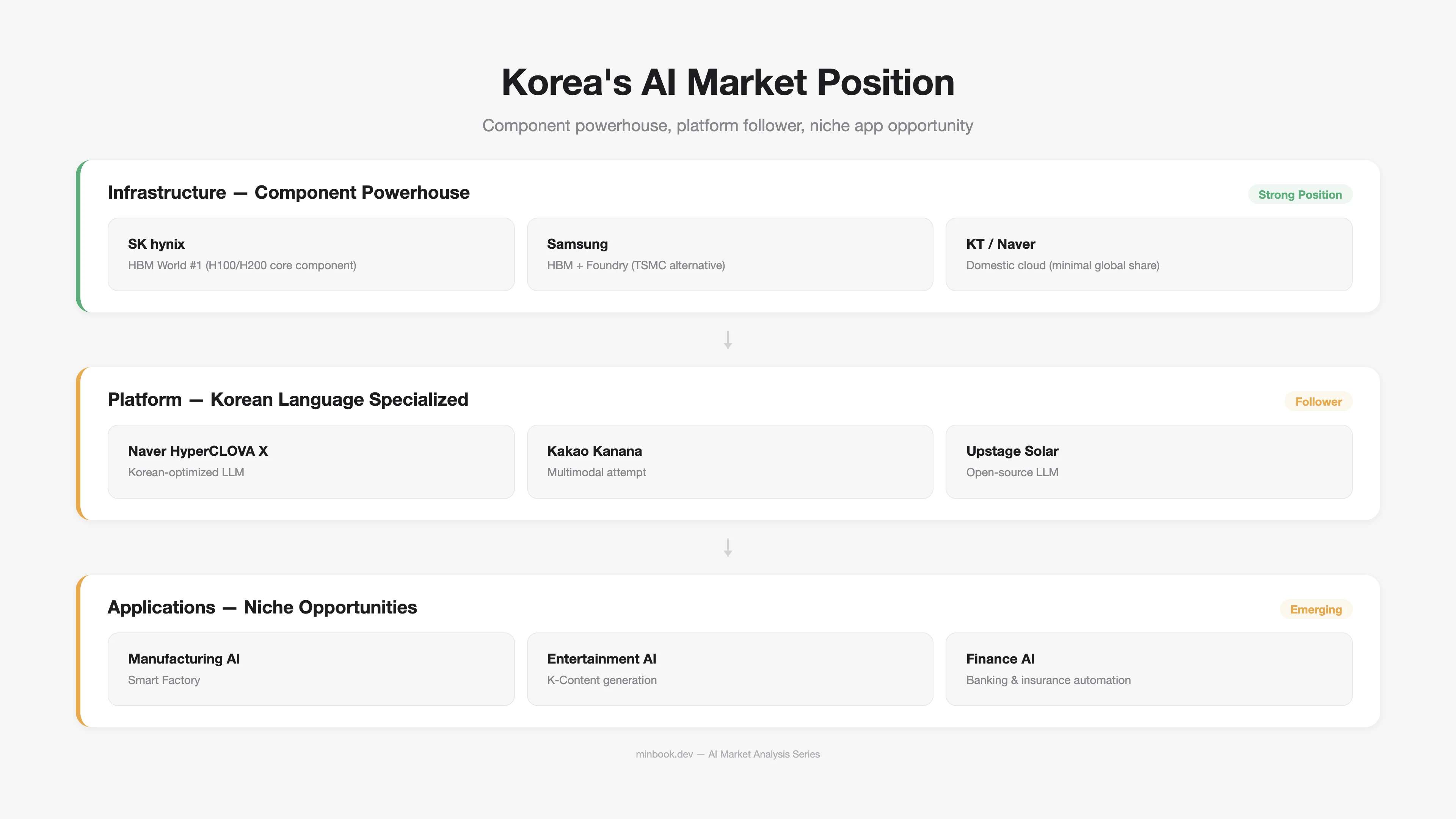

Mapping South Korea’s Position Across the AI Stack

Applying the three-layer framework from Part 1 to South Korea reveals where the country stands in each segment.

| Layer | Global Position | Korea’s Strengths | Korea’s Weaknesses |

|---|---|---|---|

| Infrastructure | Component powerhouse | HBM (SK hynix #1), Foundry (Samsung) | No GPU design capability, weak cloud infrastructure |

| Platform | Late entrant | Naver HyperCLOVA X, Kakao | Limited global competitiveness, Korean-language niche |

| Application | Niche contender | Manufacturing, semiconductor, gaming, entertainment domains | Small domestic market, immature B2B AI SaaS ecosystem |

The AI Basic Act: Opportunity or Regulation?

Overview of the Law

On January 22, 2026, the Act on the Development of Artificial Intelligence and Establishment of Trust (AI Basic Act) came into force. It is the world’s second comprehensive AI regulation after the EU AI Act.

| Item | Details |

|---|---|

| Effective Date | 2026.01.22 |

| Key Provisions | Mandatory impact assessments for high-risk AI, generative AI labeling, designation of domestic representatives |

| Scope | All AI systems operating in Korea (including foreign companies) |

| Grace Period | Approximately 1 year from enforcement (per detailed enforcement decrees) |

| Penalties | Fines up to 3% of revenue for violations |

Opportunities Created by the AI Basic Act

1. Regulatory Arbitrage Services. Companies operating globally now need to comply with both the EU AI Act and Korea’s AI Basic Act simultaneously, creating demand for compliance services. AI impact assessments, labeling, and monitoring tools could form a new B2B SaaS category.

2. “Trust-Based” AI Certification Market. Certification and audit services for AI systems that meet the impact assessment and transparency requirements mandated by the AI Basic Act. This could develop into an industry similar to existing ISO certification.

3. Korean-Language AI Data Premium. The generative AI labeling mandate requires transparency around training data sources and quality. The value of high-quality Korean-language datasets could rise accordingly.

Risks of the AI Basic Act

1. Compliance Costs for Startups. The cost of meeting impact assessment, labeling, and domestic representative requirements may fall disproportionately on early-stage startups. Large enterprises have regulatory compliance teams; startups do not.

2. Slower Innovation Velocity. AI model update cycles run on weeks, but impact assessments can take months. The gap between regulatory compliance speed and innovation speed risks eroding competitiveness.

3. Advantage to Foreign Services. If regulations are effectively enforced only against domestic companies while foreign companies evade compliance without consequence, a reverse-discrimination structure could emerge.

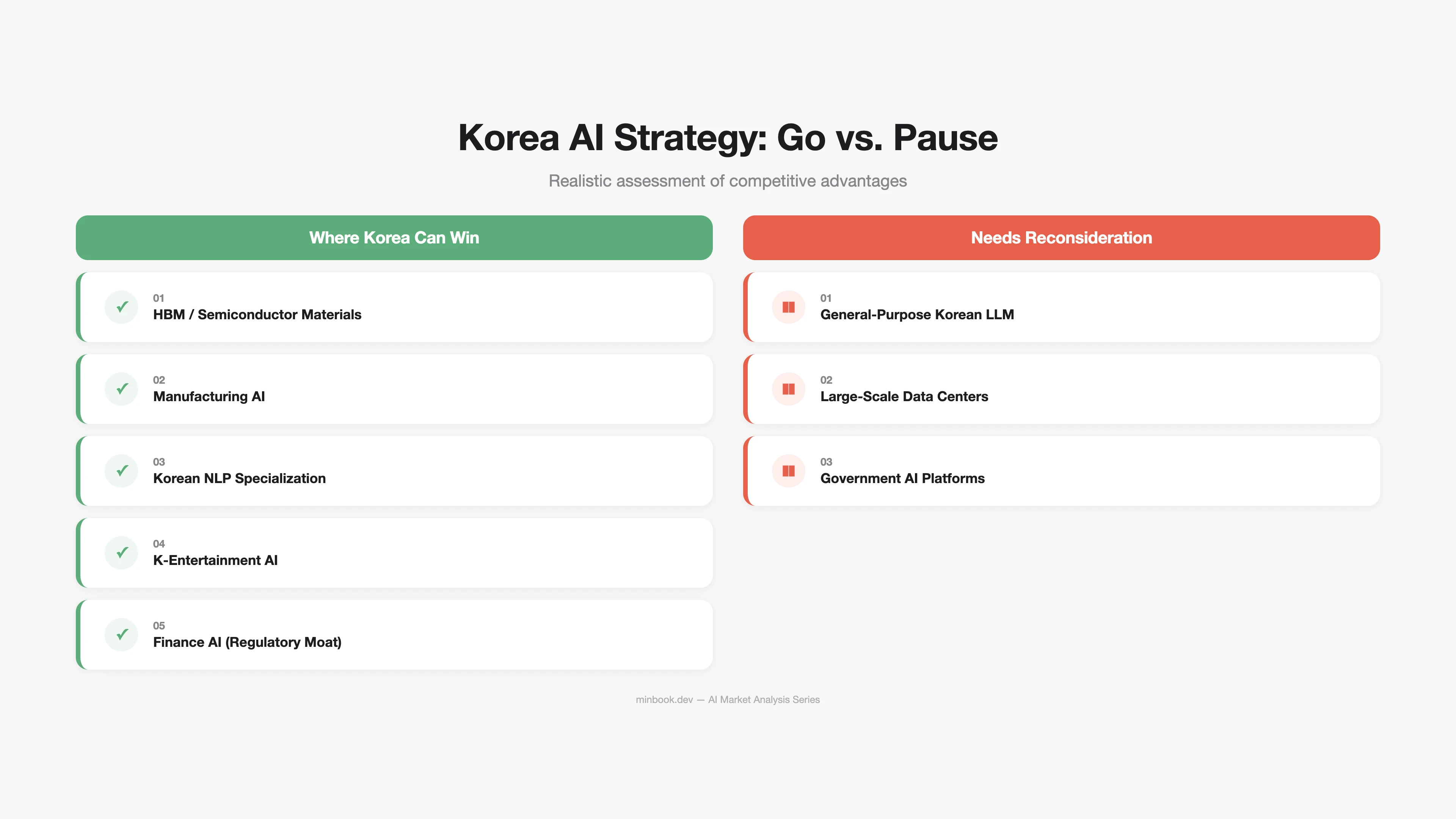

Where Korea Can Win: 5 Areas

A realistic assessment of the areas where South Korea can achieve global competitiveness in AI.

1. HBM / AI Semiconductor Materials & Components

Competitiveness: Very Strong

SK hynix holds over 50% of the global HBM3e market and maintains an exclusive supply position for NVIDIA’s next-generation GPUs. HBM is a bottleneck resource for AI infrastructure, and supply shortages are projected to continue through 2026.

| Company | Product | Global Market Share | Key Customers |

|---|---|---|---|

| SK hynix | HBM3e | ~53% | NVIDIA, AMD |

| Samsung Electronics | HBM3e | ~40% | NVIDIA, AMD, Google |

| Micron | HBM3e | ~7% | AMD |

Implication: HBM is an area where Korea is already winning. Rather than further standalone investment, a vertical integration strategy — HBM to AI accelerator packaging to testing and validation — is the path to capturing more value.

2. Manufacturing AI (Smart Factory)

Competitiveness: Strong

South Korea’s manufacturing density is among the highest in the world. Massive production facilities at Samsung Electronics, Hyundai Motor, LG, and POSCO are supported by thousands of small and medium manufacturers. The manufacturing data and domain expertise accumulated in this environment are assets that global AI companies cannot easily replicate.

Specific opportunities:

- Semiconductor yield prediction AI — Already deployed internally at Samsung Electronics and SK hynix; can be packaged as external solutions

- Automotive quality inspection AI — Built on Hyundai Motor Group’s smart factory data

- Battery manufacturing optimization — Leveraging manufacturing data from LG Energy Solution, Samsung SDI, and SK On

3. Korean / East Asian NLP Specialization

Competitiveness: Medium to Strong

GPT-4o and Claude 3.5 support Korean, but there are still performance gaps in domain-specific Korean covering law, financial regulation, and medical terminology. Opportunities in this gap include:

- Korean legal AI (case law search, contract review)

- Korean tax and accounting AI (tax code interpretation, filing automation)

- Korean language education AI (Korean learning tools for non-native speakers)

- K-content localization AI (translation + cultural context adaptation)

4. K-Entertainment AI

Competitiveness: Medium to Strong

Korea’s entertainment industry — K-pop, K-drama, gaming — has proven global demand. AI-powered content creation and management tools hold a domain advantage here.

- AI idols / virtual influencers — Already backed by investment from SM Entertainment, HYBE, and others

- Game NPC / story generation — AI applications at Nexon, NCSoft

- Real-time translation and dubbing — Improving the global distribution efficiency of K-dramas

5. Financial AI (Regulation-Specific)

Competitiveness: Medium

South Korea’s financial market is heavily regulated, making it difficult for foreign AI solutions to enter directly. This regulatory barrier itself becomes a moat.

- Banking AML/KYC automation

- Insurance underwriting AI

- Securities research automation

- Financial compliance monitoring

Areas That Need Rethinking

General-Purpose Korean LLM Development

Naver’s HyperCLOVA X, Kakao’s Kanana, and Upstage’s Solar are all developing Korean-language LLMs. But a sober assessment is warranted.

| Comparison | Global Models (GPT-4o, Claude) | Domestic Models (HyperCLOVA X, etc.) |

|---|---|---|

| Training Data | Trillions of tokens | Hundreds of billions of tokens |

| R&D Investment | $10B+/year | $100M–$500M/year |

| Korean Performance | ~90–95 level | ~92–97 level |

| Beyond Korean | 100+ languages, strong | Korean + English |

| Update Cycle | 2–4 weeks | 3–6 months |

Even with a slight edge in Korean performance, the 20–100x gap in investment makes it hard to sustain that advantage long-term. With the US and China dominating the general-purpose LLM race, it may be more realistic for Korea to focus on application-level differentiation in specific domains rather than competing on general-purpose models.

Large-Scale AI Data Center Investment

The logic of “you need data centers to do AI” is driving expanded investment in domestic AI data centers. But consider:

- Power costs: Korea’s industrial electricity rate is approximately 100 KRW/kWh (

$0.07), roughly twice as expensive as some US regions ($0.03–0.04) - Location: The land, power supply, and cooling water requirements for hyperscale data centers are constrained in Korea

- Scale: Competing with a single hyperscaler data center investment ($10B+) is impractical

What Korea needs is not “the world’s largest AI data center” but rather small-scale inference infrastructure optimized for specific workloads.

Government-Led AI Platforms

Government-led projects like “K-AI Platform” and “National AI Hub” have historically shown limited market success. During the cloud transition, initiatives like “G-Cloud” were attempted, but AWS, Azure, and GCP ultimately captured even the public sector market.

The government’s role should not be platform-building, but rather:

- Regulatory environment design (pragmatic enforcement decrees for the AI Basic Act)

- Talent development (AI engineers, data scientists)

- Data infrastructure (public data APIs, standardization)

A Strategy Framework for Korean AI Companies

The “Global Infrastructure + Korean Apps” Strategy

Korea’s optimal strategy is to participate in the global supply chain at the infrastructure layer, while attacking niches at the application layer using Korean domain expertise as the primary weapon.

| Strategy | Description | Examples |

|---|---|---|

| Infrastructure Supplier | Supply critical components to global AI infrastructure | SK hynix HBM, Samsung Foundry |

| Platform Consumer | Leverage global LLM APIs, minimize in-house development | OpenAI/Anthropic API + Korean data |

| Application Niche | Domain-specific apps built on Korean regulation, data, and expertise | Legal AI, Manufacturing AI, Financial AI |

Execution Priorities

- Short-term (6 months): Build Korean domain-specific applications on top of global LLM APIs. Prioritize data acquisition and workflow integration over in-house model development.

- Mid-term (1–2 years): AI Basic Act compliance tools; international expansion of manufacturing AI solutions (targeting Southeast Asian manufacturing markets).

- Long-term (3–5 years): Vertical integration built on HBM leadership; licensing and API commercialization of Korean domain data.

Sources

- Korea AI Basic Act — US Trade.gov, Cooley Law (2026.01), BABL AI

- SK hynix HBM Market Share — TrendForce (2025), CNBC, SK hynix FY25

- Samsung Electronics Semiconductor — Samsung Foundry Investor Presentation 2025 (PDF), Samsung FY2025 Results

- Naver HyperCLOVA X — NAVER HyperCLOVA X, CLOVA Studio

- Kakao Kanana — if(kakao)25 Conference, Kakao Q3 2025 Earnings

- Upstage Solar — Upstage Blog, Hugging Face (SOLAR-10.7B)

- Korea Power Costs — Korea Herald, S&P Global, IEA Korea 2025 (PDF)

- Korea Manufacturing AI — US Trade.gov Smart Factory, Samsung SDS AI Case Studies

- K-Entertainment AI — SM Entertainment AI Strategy (MBW), HYBE Supertone AI TTS (MBW)

- Korea Financial AI Regulation — Financial Services Commission Press Releases, Chambers & Partners AI 2025 South Korea

Related Posts

Deepfake Detection $15B — Who Are the Real Buyers?

The real buyers driving Deepfake Detection toward $15B aren't security teams — they're BFSI KYC departments. Four-SaaS breakdown, Hong Kong incident impact, and the Korean KYC 2.0 mapping through data.

The Identity Track — From Proof of Personhood to AI Agent Delegation

Proof of personhood and AI agent identity are two layers of the same track. World ID, Passkey, DID adoption curves + Defakto, t54, Indicio funding + payment network entries — the entire identity track in one piece.

SynthID vs C2PA — The Standards War in Adoption Data

The two dominant AI content watermark standards — SynthID and C2PA — adoption broken down by modality, timeline, and camp. Same trust problem at different layers, heading toward coexistence rather than displacement. Plus EU Article 50's operational gaps and compliance gaming scenarios.