The Structural Problem of AI SaaS -- What a 40% GRR Really Means

A Structure That Demands Refilling 60% Every Year

The most fundamental metric for measuring SaaS business health is GRR (Gross Revenue Retention). How many existing customers stay and continue paying the following year. Excluding expansion, it measures purely “how much existing customer revenue is retained.”

The median GRR for traditional SaaS is over 90%. In B2B SaaS benchmarks, a GRR below 85% is classified as “problematic.”

The median GRR for AI-native SaaS is 40%.

What this number means: if an AI SaaS company hits $10M ARR this year, the revenue that survives into next year without acquiring a single new customer is only $4M. The remaining $6M churns. Every year, 60% of revenue must be replaced just to maintain the status quo. Growing requires filling even more than that.

Why does this happen, and what is different about the companies that have broken this pattern.

The Data: ChartMogul AI Churn Wave Report

The core data for this analysis comes from ChartMogul’s “SaaS Retention: The AI Churn Wave” report (September 2025). It compares retention data from roughly 200 AI-native companies against approximately 2,700 B2B SaaS companies overall.

GRR Comparison: AI-native vs Traditional SaaS

| Metric | AI-native SaaS | Traditional B2B SaaS | Gap |

|---|---|---|---|

| Median GRR | 40% | 90%+ | -50%p |

| Median NRR | 48% | 105%+ | -57%p |

| Monthly Logo Churn Rate | ~12% | ~3% | 4x |

| First 90-Day Churn Rate | ~40% | ~8% | 5x |

An NRR (Net Revenue Retention) of 48% is especially alarming. Even including upsell and expansion from existing customers, more than half of the revenue disappears. In traditional SaaS, an NRR below 100% is a warning signal that “the business model has a problem.” AI SaaS sits at 48%.

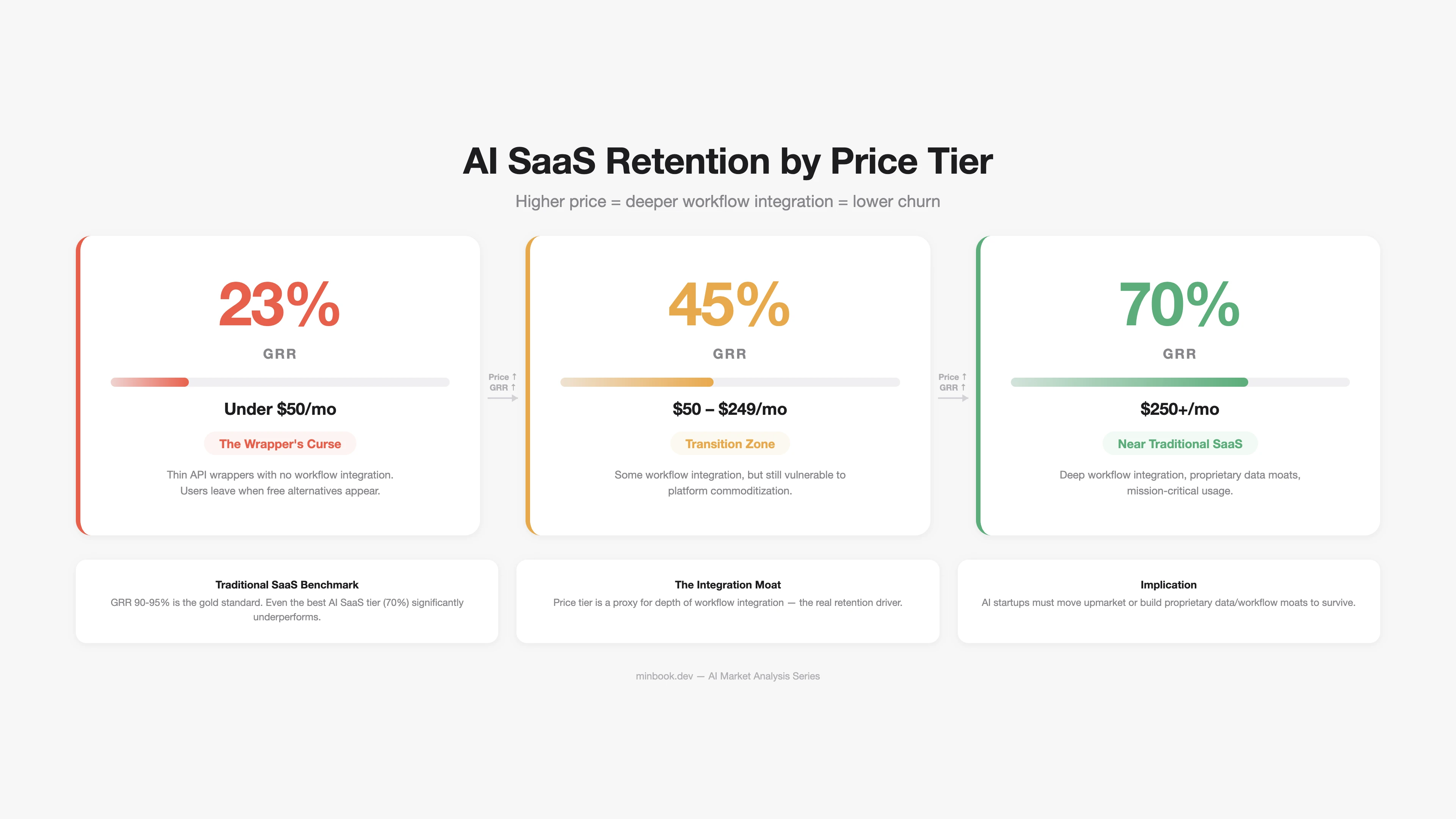

GRR by Price Tier

The most striking finding from the ChartMogul data is the GRR gap across price tiers.

| Monthly Subscription | AI-native GRR | Traditional SaaS GRR | Implication |

|---|---|---|---|

| Under $50 | 23% | ~85% | Near-total churn |

| $50—$249 | 45% | ~88% | Still critical |

| $250+ | 70% | ~93% | Approaching traditional SaaS |

The pattern is clear. The more customers pay, the less they churn. This is not simply “rich companies are too lazy to leave.” Customers paying higher prices are far more likely to have the AI tool deeply integrated into their workflows. Switching costs exist.

Conversely, a GRR of 23% for products under $50/month is essentially selling a feature for money that could be replicated for free.

Why AI SaaS GRR Is This Low

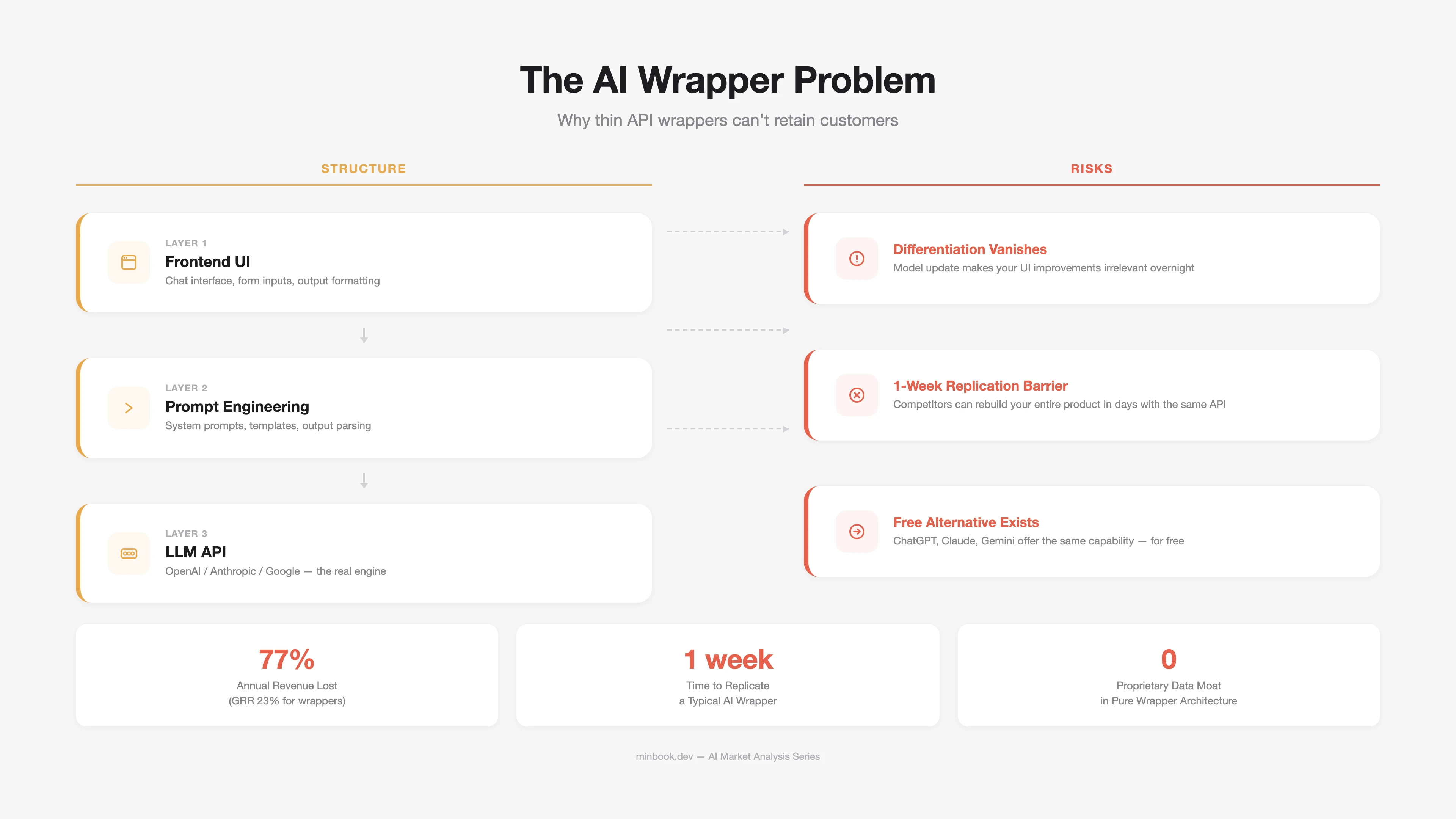

Cause 1: The Structural Limitation of “AI Wrappers”

The biggest driver is the undifferentiated API wrapper business model.

A typical AI wrapper product follows this structure:

- Build a user interface (UI)

- Call OpenAI/Anthropic APIs behind the scenes

- Add prompt engineering tailored to a specific use case

The problem is that none of these three elements constitute a defensible moat. The UI can be quickly replicated, the API is accessible to anyone, and prompt engineering can be invalidated by a model update.

A concrete example: the AI writing tools that grew explosively in 2023—2024 (Jasper, Copy.ai, etc.) saw sharp traffic declines in 2025. ChatGPT-4o began offering the same functionality for free or at low cost.

Cause 2: The “Wow to Meh” Cycle

AI products have a distinctive user experience pattern. The first encounter delivers surprise (Wow), but once limitations are discovered, disillusionment (Meh) sets in rapidly.

| Phase | Timeline | User Sentiment | Behavior |

|---|---|---|---|

| 1. Discovery | 1—7 days | ”This actually works?” | Converts to paid |

| 2. Exploration | 1—4 weeks | ”Let me try this too” | Active usage |

| 3. Hitting Limits | 1—3 months | ”Why doesn’t this work?” | Usage frequency drops |

| 4. Seeking Alternatives | 3—6 months | ”There must be something better” | Tries competitors |

| 5. Churn | 6—12 months | ”I’ll just use ChatGPT” | Cancels subscription |

This cycle explains the 40% first-90-day churn rate of AI SaaS. Users acquired through free trials or discount promotions discover limitations and leave quickly.

Cause 3: The Relentless Emergence of Free Alternatives

A unique characteristic of the AI ecosystem is that free and open-source alternatives keep appearing.

- Open-source models: Llama 3, Mistral, Qwen, DeepSeek, and others deliver performance approaching commercial models for free

- Base model feature expansion: ChatGPT, Claude, and Gemini now directly support code execution, image generation, data analysis, and file processing — weakening the raison d’etre of standalone AI SaaS

- Community tools: Open-source frameworks like Hugging Face, LangChain, and LlamaIndex enable anyone to build AI apps quickly

What Companies That Beat Churn Have in Common

Not every AI SaaS fails. Companies achieving GRR of 70% or higher exist, and they share common patterns.

Pattern 1: Workflow Embedding

Products that don’t just display AI output, but integrate deeply into existing work processes.

| Company | Domain | Workflow Integration Method | Estimated GRR |

|---|---|---|---|

| GitHub Copilot | Development | Real-time code completion inside the IDE | 70%+ |

| Harvey | Legal | Document review and contract analysis automation | 80%+ |

| EvenUp | Medical-Legal | Medical records to legal demand letters, auto-generated | 85%+ |

| Cursor | Development | AI-native IDE (entire development environment) | 75%+ |

What these companies share: integration to the point where not using the AI makes the work itself painful. Not simply “offering AI features,” but creating switching costs where “without AI, you have to revert to the old way.”

Pattern 2: Proprietary Data/Models

Companies that hold domain-specific data and fine-tuned models on top of general-purpose LLM APIs.

- Bloomberg GPT-style finance-specialized models

- Diagnostic AI trained on medical data

- Legal AI integrated with case law databases

These have differentiation where “swapping out the OpenAI API cannot produce the same results.” Data is the moat.

Pattern 3: High Price + High Value

It is no accident that AI products priced at $250+/month achieve 70% GRR. Higher pricing:

- Filters in only customers who made a serious purchasing decision (tire-kicker filtering)

- Secures the margin needed to invest in onboarding and customer success

- Enables value-based pricing rather than usage-based (justified by the value of the output)

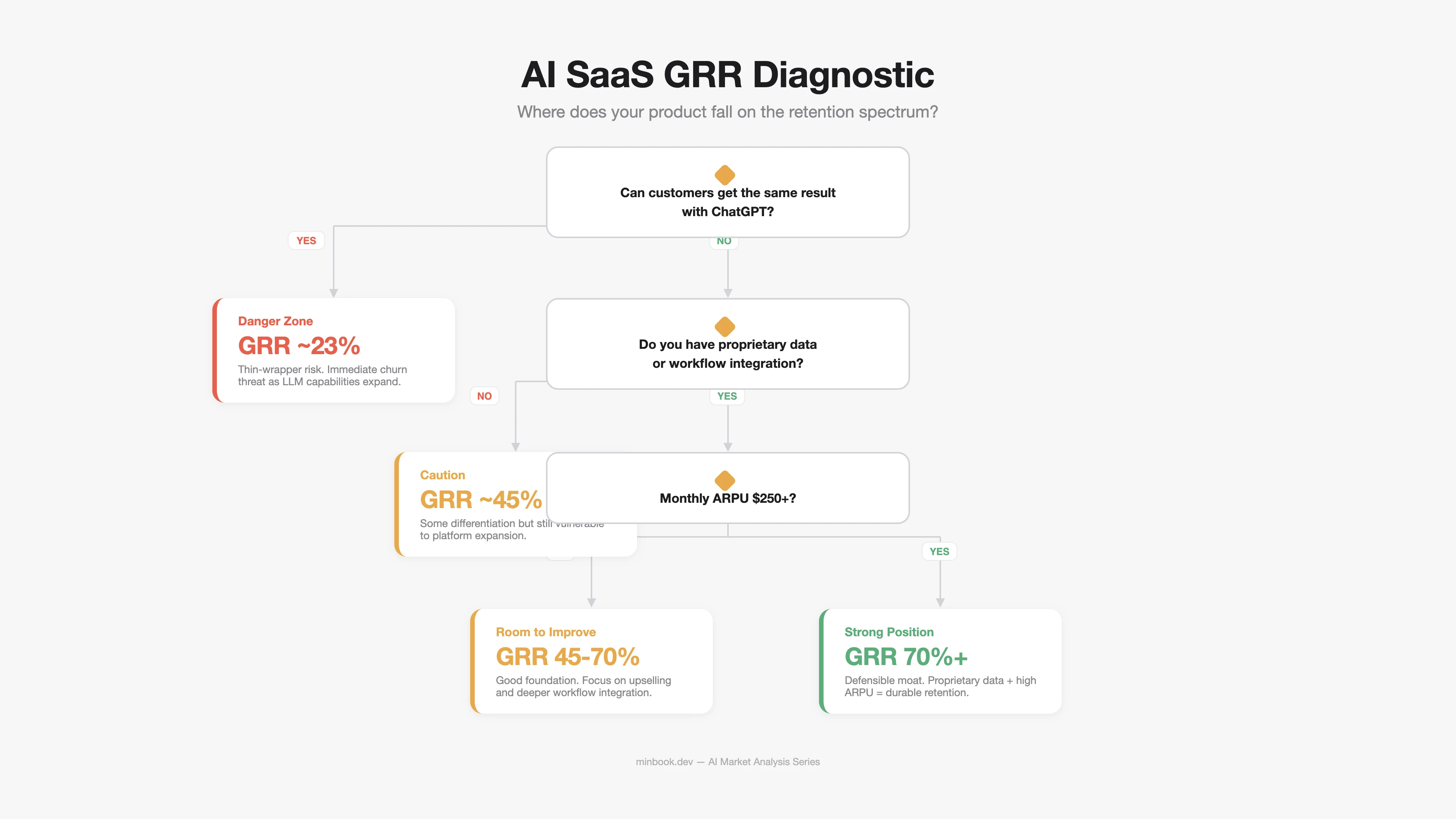

A Checklist for AI SaaS Builders

If you are building or operating an AI SaaS, answer the following questions.

| Question | Danger Signal | Healthy Signal |

|---|---|---|

| How would customers get the same result without our product? | ”Can do something similar with ChatGPT" | "3 hours manually, can’t be automated” |

| What is our core differentiation? | ”Nice UI” / “Good prompts" | "Proprietary data” / “Workflow integration” |

| What happens when the base model updates? | ”Our differentiation disappears" | "Our performance actually improves” |

| Monthly ARPU? | Under $50 | $250+ |

| 90-day retention? | Under 60% | 75%+ |

Investor/Observer Perspective: An AI SaaS Evaluation Framework

When evaluating AI SaaS companies, applying traditional SaaS multiples as-is is dangerous.

| Metric | Traditional SaaS Standard | Caution When Applied to AI SaaS |

|---|---|---|

| ARR Growth Rate | Higher is better | Check dependency on new customers (if GRR is low, growth is “running on a treadmill”) |

| NRR | 120%+ = excellent | AI SaaS median is 48% — churn exceeds expansion |

| CAC Payback | Under 12 months = excellent | At 40% GRR, customers churn before CAC is recovered |

| Rule of 40 | Growth rate + margin ≥ 40% | GPU costs structurally compress margins |

The key: don’t just look at AI SaaS ARR growth. GRR, first-90-day retention, and ARPU must be verified. Even at $50M ARR, a 40% GRR means $30M must be replaced next year just to stay flat.

Sources

- ChartMogul AI Churn Wave Report — ChartMogul “SaaS Retention: The AI Churn Wave” (Sep 2025), based on data from ~200 AI-native and ~2,700 B2B SaaS companies

- Growth Unhinged — Kyle Poyar, “The AI Churn Wave” Analysis (2025)

- AI Wrapper Churn Cases — Jasper Valuation Writedown (Maginative), Contrary Research

- GitHub Copilot Retention — TechCrunch (20M users), CIO Dive

- Harvey AI — Series C $100M (Sequoia Lead), Law.com Coverage (2025)

- EvenUp — Series D $200M, Forbes Coverage (2025)

- Cursor — Anysphere $9.9B, $500M+ ARR (TechCrunch)

- Open-Source Model Performance — Chatbot Arena Leaderboard (LMSYS), Epoch AI Benchmark Tracking

- SaaS Benchmarks — Bessemer Cloud Index, OpenView SaaS Benchmarks 2025

- AI SaaS Cost Structure — a16z “Who’s Making Money in AI?” (2025), Battery Ventures Cloud Software Report

Related Posts

Solo Builder OSS Monetization - Is It Possible Without Enterprise Sales?

OSS monetization framework for solo builders. Outlines a 5-stage strategy using the 'What (Free) - How (Paid)' model to generate revenue without enterprise sales or managed infrastructure.

Monetizing AI Infrastructure - Hugging Face, Qdrant, Weaviate

Analysis of AI infrastructure monetization. Details the 'software free, operations paid' model, where revenue is driven by GPU compute hours and data storage volume in the AI stack.

How AI Observability Platforms Make Money -- Langfuse and Dify

Analysis of Langfuse and Dify's open-source monetization. Explains why observability layers are structurally superior to frameworks due to higher switching costs and continuous usage.